Inflation - Inflation

|

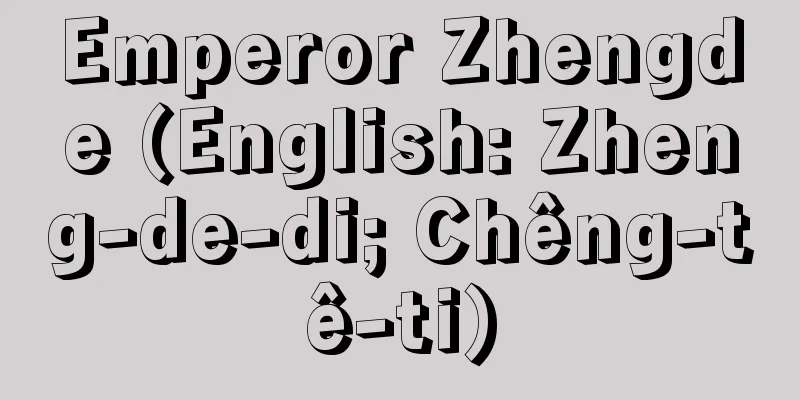

The phenomenon in which prices continue to rise for a certain period of time. Three types of inflation that are particularly problematic in the economy are malignant inflation, chronic inflation that became common after World War II, and global inflation that arose as a result of the oil shock at the end of 1973. [Tetsuya Hitosugi] Malignant inflationDuring wartime and postwar periods of chaos, when prices soar due to excessive issuance of inconvertible paper money in excess of the amount needed for commodity circulation, this is called pernicious inflation or hyperinflation. For example, in Japan immediately after World War II, production capacity was halved due to air raids, and demand, which had been suppressed by price controls and rationing, exploded due to the defeat. This was caused by the issuance of a large amount of Bank of Japan notes in the name of compensation for cancellations of orders to munitions companies. Furthermore, the issuance of Reconstruction Finance Bonds underwritten by the Bank of Japan spread pernicious inflation, known as the Reconstruction Inflation. Famous historical examples of inflation caused by excessive issuance of inconvertible paper money include France during the Revolution with Assinnat paper money, America during the Civil War with Greenbacks (a colloquial name for American paper money), Germany after both world wars with Mark paper money, and Eastern Europe after World War II. Inflation causes great damage to society: (1) wages always rise only after prices have risen, which harms workers, (2) it threatens people who live on fixed incomes, such as rentiers, pensioners, and households on welfare, (3) people lose confidence in money, so savings are cut and exchange becomes more prevalent, which fuels inflation even more, (4) production is hindered because value increases faster in the distribution process than in the production process, allowing black market merchants and speculators to run rampant, (5) people are unable to forecast the future, so capital investment is cut, which fuels further inflation through stagnation of productivity, and (6) this situation leads to a decadence of the human spirit, the prevalence of hedonism, and the destruction of social morality, etc. In order to contain this kind of malignant inflation, it is necessary above all to suppress monetary demand and restore the balance with production. For this purpose, possible measures include currency reform (denomination, etc.), deposit moratorium, super-balanced budget, and increased savings. The world's highest denomination was the 1/40th revaluation (1 revaluation is 10 to the 28th power) implemented in Hungary after World War II. Policies such as super-balanced budget through tax increases and increased savings are called disinflation. This was advocated by the British Labour government after World War II, and aimed to stabilize prices at a plateau so as not to fall into deflation due to a sudden tightening of monetary policy. In Japan, the Dodge Line implemented in 1949 (Showa 24) is said to be an example of this. [Tetsuya Hitosugi] Chronic InflationApart from malignant inflation, major countries have been plagued by chronic or "creeping" inflation since the end of World War II, in which prices rise by about 4-5% per year. This type of inflation in the West is generally called cost inflation. With full employment and powerful labor unions as a backdrop, money wages rise faster than the rate of increase in labor productivity, prices are raised to cover this, and this rise in prices causes further wage increases, resulting in inflation. Income policies are considered as a policy to curb this type of cost inflation, but few countries have been successful in implementing them. [Tetsuya Hitosugi] Productivity Growth Rate Gap InflationJapan also saw a rapid rise in consumer prices from around 1960, but the situation was very different from that in Europe and the United States. In other words, while wholesale prices and consumer prices rose in tandem in Europe and the United States, in Japan wholesale prices remained extremely stable until around 1972, while only consumer prices soared. If cost inflation had occurred simultaneously in the producer goods industry and consumer goods industry, the prices of both goods would have risen in tandem, as in Europe and the United States. The chronic inflation in Japan, at least until around 1972, can be called productivity growth rate differential inflation. In other words, there was a huge demand for funds due to high economic growth, but the self-financing ability of companies was extremely weak, and they were largely dependent on loans from financial institutions. Since financial institutions that supplied this funds had limited supply capacity, they concentrated their loans on large companies, which had low risk of default and low lending costs, and did not lend easily to small and medium-sized enterprises. Thus, large companies that could borrow made capital investments to increase labor productivity and absorbed wage increases, but small and medium-sized enterprises that could not borrow found it difficult to increase labor productivity and were forced to cover wage increases with increases in product prices. As a result, the downward trend in prices of products made by large companies and the upward trend in prices of products made by small and medium-sized enterprises offset each other, and wholesale prices remained stable. Meanwhile, consumer prices, including those in the service industry, where the proportion of products made by small and medium-sized enterprises is large and it is essentially difficult to increase productivity, continued to rise. Thus, Japan's chronic inflation was thought to be based on the disparity in productivity growth rates between large and small companies. [Tetsuya Hitosugi] Fiscal InflationHowever, it is also pointed out that a kind of fiscal inflation was taking place during that time. That is, one year after the first deficit bonds were issued in February 1966, the Bank of Japan implemented a monetary policy under which it would unconditionally purchase any government bonds held by banks that had been issued one year after they were issued. This was a means of rescuing banks that were unable to sell their government bonds, but in the end it was nothing more than a government bond issue underwritten by the Bank of Japan one year late, which led to an increase in private currency, and it cannot be denied that this contributed to inflation until it was temporarily halted under measures to curb aggregate demand after the oil crisis. [Tetsuya Hitosugi] The challenge of monetarismIncidentally, since the 1960s, a new economic ideology known as monetarism has been actively challenging Keynesianism, which was thought to dominate the fiscal and monetary policies of advanced capitalist countries. Monetarists also have a unique interpretation of the "impending inflation." If we assume in that there is no increase in labor productivity and plot the unemployment rate on the horizontal axis and the rate of increase in prices (money wages) on the vertical axis, we empirically obtain a downward-sloping curve A. This is the so-called Phillips curve. When the unemployment rate in the labor market is high, there is little upward pressure on wages, and therefore prices do not rise. If the unemployment rate is low, rising wages lead to rising prices, so this curve indicates that there is a trade-off between unemployment and prices. Now, starting from point a , if we increase government spending etc. to reduce unemployment, we must accept a certain degree of price rise as compensation. This is the Keynesian position, and let's assume that this is represented by point b . Monetarism introduces expectations into this. The workers who increased their labor supply from a to b were actually hired because of the expectation that wages would rise 5% and prices would rise 0%, and therefore real wages would rise 5%. However, if wages rise and this causes a 5% rise in prices, workers will soon realize that real wages will not rise at all. Then labor supply will decrease and point c will be established. On the other hand, if policies to reduce the unemployment rate are continued and larger fiscal expenditures are invested, it will go to point d , where the wage increase rate is 10%. Then workers will increase their labor supply, expecting a 10% wage increase, a 5% rise in prices, and therefore a 5% rise in real wages. Then the Phillips curve will shift upward to B. If we interpret it this way, if we try to reduce the unemployment rate to a level lower than point a through Keynesian policies, wages and prices will continue to rise indefinitely. This is the real inflation, which is nothing other than a product of Keynesianism, and in order to suppress inflation, the unemployment rate at point a (the natural unemployment rate) should be maintained. There are many other points to be discussed regarding monetarism, and there are many theoretical problems with it, but it does explain to some extent the fact that the Phillips curves of major countries became vertical or sloped upward to the right around the time of the oil shock. [Tetsuya Hitosugi] Inflation caused by the oil shockThe shock of oil supply restrictions and oil price hikes triggered by the Yom Kippur War in October 1973 spread throughout the world, causing inflation and recession. However, it should be noted that in Japan, a considerable accelerated inflation had already been occurring since around 1972 (Showa 47) before the oil shock. The first cause was excess liquidity. Since the Nixon Statement in August 1971, foreign currency flowed into Japan in anticipation of profits from the revaluation of the yen, reaching 10 billion dollars. Even after the revaluation of the yen in December of the same year, it remained in the country, becoming what is called excess liquidity, and was used to fund various types of speculation. The second was monetary easing. The authorities, predicting a recession due to the Nixon Shock, implemented significant monetary easing, but the economy had already overcome the recession by January 1972, and surplus funds flowed into speculation. This could be called a typical credit inflation. The third was the recession cartel. As mentioned above, the government, predicting a recession, approved recession cartels in the steel, petrochemical, and other industries, but the economy was already booming at the time, and this resulted in soaring product prices. Fourth, the publication of the "Japan Archipelago Remodeling Theory" created a mood of speculation and inflation, including land buying up. The combination of these policy mistakes led to a significant rise in prices, which was then followed by the oil crisis. First, the oil shock had a ripple effect on developed countries, where the price of imported raw materials and fuels rose, product prices rose, demand fell, and production stagnated. Many countries implemented demand-suppression measures to curb inflation, which exacerbated the above process and caused a global recession. Compared to the previous situation of economic boom = price rise, the abnormal situation of economic recession = price rise appeared, and this is called stagflation. Second, oil-producing countries received huge income transfers from oil-importing countries, which led to increased imports of industrial products (which were already expensive due to high costs) from developed countries, raising prices in the oil-producing countries. However, this itself reduced the real purchasing power of oil revenues, creating a vicious cycle that accelerated the rise in oil prices. Third, in developing countries that do not produce oil, the soaring prices of imported goods from developed countries caused import inflation, resulting in a deficit in the balance of payments. As long as the oil dollars that flow from oil-producing countries to developed countries are lent to non-oil-producing developing countries, this deficit can be covered, but there is a natural limit to how much they can do, and non-oil-producing developing countries are becoming increasingly uneasy about their creditworthiness. This leads to a shortage of foreign currency, which leads to a shortage of imported necessities, which leads to stagnation in production, and inflation is becoming more common. Fourthly, this situation has spread to socialist countries, causing a significant rise in prices and a stagnation or decline in living standards. [Tetsuya Hitosugi] Imported and domestic inflationIncidentally, inflation in a country can be divided into import inflation and domestic inflation. If the price of imported goods becomes higher in overseas markets, their domestic prices will rise even if the exchange rate remains unchanged. Also, even if the price in overseas markets remains unchanged, if the exchange rate falls, the domestic price of imported goods will rise. The latter is called exchange rate inflation, and inflation in Argentina is said to be a typical example of this. Together, the two are called import inflation. Let's say that the imported goods that have become more expensive in this way are raw materials and fuels for industry. When the price of imported raw materials used by an upstream factory rises, the factory raises the price of its products by the same amount and sells them to a midstream factory, which then raises the price of its products by the same amount and sells them to a downstream factory... In this way, the price of consumer goods produced by downstream factories will only rise slightly. Furthermore, if upstream factories can offset the price increase of imported goods by saving energy or other means, the price of consumer goods will not rise at all. This is the case when there is no domestic inflation. Next, let's say that an upstream factory raises the price of its products by the same rate as the price increase of imported raw materials. In other words, the added value (wages and profits) will also increase. If midstream factories follow this example and raise the price of their products by increasing not only the price increase of raw materials but also the added value, and sell them downstream... the price of consumer goods will rise to the same rate as the price increase of imported goods. This is domestic inflation. This is said to be the case during Japan's first oil shock (1973) and the inflation in the United States, but it has been pointed out that there was no domestic inflation during Japan's second oil shock (1978). In this way, modern inflation has become a phenomenon that affects all aspects of the economic system, including international prices, exchange rates, wages, profits, finances, banking, and politics. [Tetsuya Hitosugi] "The Political Economy of Inflation" edited by F. Hirsch and J.H. Goldthorpe, supervised translation by Shigeto Tsuru (1982, Nihon Keizai Shimbun) [References] | | | | | | | | | | | |©Shogakukan "> The Phillips Curve (The relationship between unemployment and prices) Source: Shogakukan Encyclopedia Nipponica About Encyclopedia Nipponica Information | Legend |

|

ある程度の長期間にわたって物価が上昇し続ける現象。経済上とくに問題となるのは、悪性インフレーション、第二次世界大戦後一般化した慢性的インフレーション、そして1973年末のオイル・ショックに基づいて発生した世界的インフレーションの三つであろう。 [一杉哲也] 悪性インフレーション戦時・戦後の混乱期などに、商品流通に必要な量以上に不換紙幣が乱発されて物価暴騰が起こったとき、これを悪性インフレーションまたは超インフレーションという。たとえば第二次世界大戦直後の日本のそれは、空襲などによって生産能力が半減し、かつ曲がりなりにも物価統制、配給制によって抑えられていた需要が敗戦によって爆発し、そこへ軍需会社への注文取消しに対する補償という名目で多額の日本銀行券が増発されたためにまず起こった。さらに復興金融金庫が日本銀行引受けで復興金融債を発行したことが、復金インフレーションとよばれる悪性インフレーションを広げた。このように不換紙幣の乱発がもとでインフレーションとなった歴史上有名な例としては、アッシニャ紙幣による大革命期のフランス、グリーンバック(アメリカ紙幣の俗称)による南北戦争期のアメリカ、マルク紙幣による両大戦後のドイツ、第二次世界大戦後の東欧などがある。 インフレーションは社会に甚大な被害を与える。すなわち、(1)賃金はつねに物価に遅れてのみ上昇するから、勤労者に被害を与える、(2)金利生活者、年金生活者、生活保護世帯など、貨幣額が固定した収入で生活する人々を脅かす、(3)貨幣に対する信用がなくなるため貯蓄がなされず、換物行為が盛んとなり、これがいっそうインフレーションをあおる、(4)生産過程におけるより流通過程での価値増殖のほうが速くなるため生産が阻害され、闇(やみ)商人、投機者の跳梁(ちょうりょう)を許すことになる、(5)将来の見通しがたてられなくなるため設備投資などが行われず、それが生産性の停滞を通じていっそうのインフレーションをあおる、(6)こうした事態から、人心の退廃、刹那(せつな)主義の横行を招き、社会道徳が破壊される、等々である。 こうした悪性インフレーションを収めるためには、なによりも貨幣的需要を抑えて生産とのバランスを回復させることが必要であり、そのためには通貨改革(デノミネーションなど)、預金封鎖(モラトリアム)、超均衡財政、貯蓄増強などが考えられる。デノミネーションとしては、第二次世界大戦後のハンガリーで行われた40穣(じょう)分の1(1穣は10の28乗)の切上げが、世界最高であろう。増税による超均衡財政、貯蓄増強などによる政策はディスインフレーションdisinflationとよばれる。これは第二次世界大戦後イギリス労働党内閣が唱えたもので、急激な引締めでデフレーションに陥らないよう、高原状に物価を安定させることをねらったものである。日本でも、1949年(昭和24)に施策されたドッジ・ラインがこれにあたるとされる。 [一杉哲也] 慢性的インフレーション悪性インフレーションとは別に、第二次世界大戦後、主要国は年4~5%程度ずつ物価が上昇する慢性的インフレーションないし「しのびよるインフレーション」creeping inflationに悩まされてきた。欧米におけるこのインフレーションは、一般にコスト・インフレーションcost inflationといわれている。それは完全雇用状態と強力な労働組合とを背景として、貨幣賃金が労働生産性の上昇率を上回って上昇し、それをカバーするために価格が引き上げられ、その物価上昇がさらに賃金引上げの原因となる形でインフレーションが進行するものである。このようなコスト・インフレーションを抑えるための政策としては所得政策が考えられるが、各国ともほとんどこれには成功しなかった。 [一杉哲也] 生産性上昇率格差インフレーション日本でも1960年(昭和35)ごろから消費者物価の上昇が急激となったが、これを欧米と比べると様相がきわめて異なっていた。すなわち、欧米では卸売物価と消費者物価が並行して上がっていたのに、日本では卸売物価は1972年ごろまではきわめて安定しており、消費者物価だけが高騰していた。もし生産財産業と消費財産業において同時にコスト・インフレーションが起こっていたなら、欧米と同様に両物価は並行して上がったはずである。 日本の少なくとも1972年ごろまでの慢性的インフレーションは、生産性上昇率格差インフレーションといいうるであろう。すなわち、高度成長のために莫大(ばくだい)な資金需要が存在するが、企業における自己資金調達能力はきわめて弱く、金融機関の貸出に依存すること大である。これを供給する金融機関としては、その供給力に限界がある以上、貸倒れの危険の少ない、貸付コストの安い相手、すなわち大企業に集中して貸し付け、中小企業には容易に貸し付けない。かくて、借入のできる大企業は、設備投資を行って労働生産性を高め、これで賃金上昇を吸収していったが、借入のできない中小企業では、労働生産性を上げることが困難なため、いきおい製品価格の上昇で賃金引上げを賄わざるをえなかった。この結果、大企業製品の価格低下傾向と中小企業製品の価格上昇傾向とが相殺して、卸売物価は安定していた。一方、中小企業製品の比重が大きく、かつ本質的に生産性を上げることの困難なサービス業を含む消費者物価は上昇を続けることとなった。こうして日本の慢性的インフレーションは、大企業と中小企業との生産性上昇率に格差があることに基づくと考えられた。 [一杉哲也] 財政インフレーションしかしその間、一種の財政インフレーションが進行していたことも指摘される。すなわち、戦後初めて赤字公債が発行された1966年2月から1年ののち、発行後1年たった銀行保有の国債は日本銀行が無条件に買い入れるという金融政策が行われることになった。これは保有国債を売却できない銀行の救済手段であったが、結果的には1年遅れの日本銀行引受けによる国債発行にほかならず、その分だけ民間の通貨が増大することとなり、オイル・ショック後の総需要抑制策の下に一時停止されるまで、インフレーションを助長したことは否定できない。 [一杉哲也] マネタリズムの挑戦ところで、先進資本主義国の財政・金融政策を支配しているとされたケインズ主義に対して、1960年代からマネタリズムといわれる新しい経済思想の挑戦が盛んになってきたが、マネタリストらは「しのびよるインフレーション」に対しても独特の解釈を与える。 いまにおいて、労働生産性上昇がないと仮定し、横軸に失業率、縦軸に物価(貨幣賃金)上昇率を目盛ると、経験的に右下がりの曲線Aが得られる。いわゆるフィリップス曲線である。労働市場で失業率が高いと賃金上昇圧力が低く、したがって物価も上がらない。失業率が低ければ賃金上昇→物価上昇となるので、失業と物価とがトレード・オフ(二者択一)の関係にあるということを、この曲線は意味する。さて、a点から出発し、失業を減らすために財政支出などを増やせば、その代償としてある程度の物価上昇は容認しなければならない。これがケインズ主義の立場であり、それがb点で示されていたとしよう。 マネタリズムは、これに予想を導入する。aからbまで労働供給を増やした労働者は、実は賃金上昇5%・物価上昇ゼロ、したがって実質賃金5%上昇という予想につられて雇われたのだとする。しかし賃金が上昇して、それが物価上昇5%を引き起こすと、労働者はやがて実質賃金上昇がゼロであることに気づく。すると労働供給は減少してc点が成立するであろう。一方、失業率を減らそうという政策が続けられ、より大きな財政支出が投下されるならば、d点すなわち賃金上昇率10%のところへゆく。すると労働者は、賃金上昇10%・物価上昇5%、したがって実質賃金上昇5%を予想して、労働供給を増やすであろう。するとフィリップス曲線は上にシフトしてBとなる。こう解釈してみると、a点より少ない失業率へケインズ主義政策によって減らそうとすると、賃金→物価の際限ない上昇が続くだけになる。これが現実のインフレーションであり、それはケインズ主義の所産にほかならず、インフレーションを抑えるためにはa点の失業率(自然失業率)を保つべきであるとする。 マネタリズムの論点はこのほか多岐にわたっており、理論的にも多くの問題点があるが、オイル・ショック前後にかけて、主要国のフィリップス曲線が垂直になったり、右上がりになったりしている事実を、ある程度説明している。 [一杉哲也] オイル・ショックによるインフレーション1973年10月、第四次中東戦争に端を発した石油供給制限と石油価格引上げのショックは、全世界に波及してインフレーションと不況を巻き起こした。しかし日本では、オイル・ショック以前にすでにかなりの加速度的インフレーションが1972年(昭和47)ごろから起こっていたことに注意しなければならない。その原因の第一は過剰流動性である。1971年8月のニクソン声明以来、円切上げによる利益を見込んで日本に流入した外貨は100億ドルに達し、同年12月の円切上げ後も国内にとどまって、いわゆる過剰流動性となり、各種投機の資金に用いられた。第二は金融緩和である。ニクソン・ショックによって不況を予測した当局が大幅な金融緩和を行ったが、景気は1972年1月には早くも不況を脱し、余裕資金は投機に向かって流れた。典型的な信用インフレーションといえよう。第三は不況カルテルである。前記のように不況を予測した政府が、鉄鋼、石油化学などの不況カルテルを認めたが、時すでに好況期で、それら製品価格の高騰を招く結果となった。第四は「日本列島改造論」の発表であり、これが土地買占めをはじめとする投機とインフレーションのムードをつくることになった。以上のような政策ミスが重なって、かなり物価が上昇していたところへオイル・ショックが追い討ちをかけたわけである。 オイル・ショックは、第一に、先進国に輸入原燃料価格上昇→製品価格上昇→需要減少→生産停滞という波及を生じた。多くの国がインフレーションを抑えるために需要抑制策を強行したことが、前記の過程をさらに深刻化させ、世界的な不況が現出した。従来の好況=物価上昇の事態に比べて、不況=物価上昇の異常事態が現れたので、これをスタグフレーションstagflationという。第二に、産油国には石油輸入国から巨大な所得移転が生じ、それが先進工業国からの工業製品(それはすでにコスト高によって高騰している)輸入増をもたらして、産油国の物価を上昇させる。ところが、それ自体が石油収入の実質購買力を減らすから、石油価格上昇を加速化することになるという悪循環が生じた。第三に、石油を産出しない発展途上国では、先進国からの輸入品の高騰が輸入インフレーションを引き起こし、国際収支の赤字が発生した。石油産出国→先進国と流れるオイル・ダラーが非産油途上国へ貸し付けられる限り、この赤字は穴埋めされるが、それにはおのずから限界があり、非産油途上国の信用不安は募る一方である。そして外貨不足→輸入必需品不足→生産停滞→インフレーションが一般化している。第四に、こうした事態が社会主義諸国にも波及して、物価上昇と生活水準の停滞ないし低下が著しい。 [一杉哲也] 輸入インフレーションと国産インフレーションところで、ある国のインフレーションは、輸入インフレーションと国産インフレーションに分けることができる。いま輸入品が海外市場で高くなれば、為替(かわせ)相場が不変でも、その国内価格は高くなる。また、海外市場での価格が不変でも、為替相場が下落すれば、輸入品の国内価格は高くなる。後者が為替インフレーションといわれるもので、アルゼンチンのインフレーションなどがこの典型といわれる。両者をあわせて輸入インフレーションという。 こうして高くなった輸入品が産業用原燃料であったとしよう。川上の工場で使う輸入原料が値上りしたとき、その値上り分だけ製品価格を上げて川中の工場に売り、そこも値上り分だけ製品価格を上げて川下の工場に売る……という形ならば、川下の工場が生産する消費財価格の上昇は、軽微にとどまるであろう。さらに川上の工場が、省エネルギーなどによって輸入品の値上り分を相殺できれば、消費財価格はまったく上がらない。これは国産インフレーションがない場合である。次に、川上の工場で輸入原料の値上り率だけ製品価格を上げたとしよう。つまり付加価値(賃金と利潤)も上げてしまうのである。川中の工場もこれに倣(なら)って、原材料の値上りだけでなく、付加価値も上げる形で製品価格を上昇させて川下に売る……とやっていけば、消費財価格は輸入品値上り率に等しく上がってしまう。これが国産インフレーションである。日本の第一次オイル・ショック時(1973)や、アメリカのインフレーションがこれであるとされ、日本の第二次オイル・ショック時(1978)には国産インフレーションがなかったことが指摘されている。 このように現代におけるインフレーションは、国際価格、為替相場、賃金、利潤、財政、金融、政治など、経済体制のすべての局面にかかわる現象となっている。 [一杉哲也] 『F・ハーシュ、J・H・ゴールドソープ編、都留重人監訳『インフレーションの政治経済学』(1982・日本経済新聞社)』 [参照項目] | | | | | | | | | | | |©Shogakukan"> フィリップス曲線(失業と物価とがトレー… 出典 小学館 日本大百科全書(ニッポニカ)日本大百科全書(ニッポニカ)について 情報 | 凡例 |

Recommend

Employee stock ownership plan - Employees' holding system

An internal system where a company encourages emp...

mechanics institutes

… The Industrial Revolution, which began in Engla...

Gion execution diary - Gion execution diary

This is the common name for the diaries of the ex...

Kamo clan

An ancient clan. Also called Kamo or Kamo, clans ...

Ikue no Yasumaro

...Later, in February 754, he played a major role...

Underdrainage (underdrainage)

Underground drainage is carried out using suction ...

Ewell

…a city in the southeast of England, Surrey. It m...

MyEroBar

A Czech female writer. Initially, she wrote works ...

Kambalda

…The state is particularly important as a produce...

Ouyang Xun

A representative calligrapher of the Tang Dynasty...

Kada - Kada

…In the Mamluk dynasty, four qaḍāts representing ...

MTBF - MTBF

Mean time between failures. The average time betwe...

Cocoon Certification

This is an inspection of cocoon quality to ensure ...

Shiruko - sweet red bean soup

Azuki bean paste is thinned with water, sugar is ...

《Kikaigashima》

...The name of a Noh piece. The Kita school calls...