Exchange - exchange (English spelling)

|

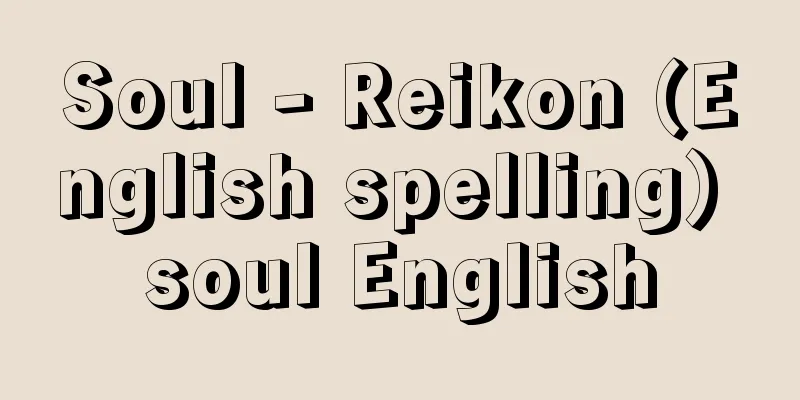

It is a mechanism for settling monetary claims and obligations between people in different locations, or transferring funds, through a third party financial institution, without transporting cash. For financial institutions, foreign exchange operations are considered one of their unique businesses, along with deposits and loans. [Kazuo Ota] historyThis system of foreign exchange began in Europe in the 12th century in cities along the Mediterranean coast, mainly in Italy, by money changers known as bancos. At the time, Italian commerce was developing remarkably and trade was thriving, but transporting currency to settle transactions between distant locations was inconvenient and dangerous. Furthermore, foreign exchange developed further with the increase in long-distance transactions resulting from the mass movement of people and goods during the Crusades in the 12th and 13th centuries. The origin of foreign exchange in Japan can be traced back to the Kamakura period. Initially, it was called "kawashi," and the system involved a client handing over money or rice to a warifu (banknote exchanger) and receiving a bill of exchange called a warifu, which the client would then hand over to the payer at the designated payment location and receive the money or rice in return. In the Edo period, "Edo foreign exchange," which connected the major consumer city of Edo with the national commercial center of Osaka to settle funds, developed rapidly, and the prototype of today's foreign exchange system was completed. Foreign exchange transactions in this period were carried out by money changers, and in 1691 (Genroku 4), the so-called Go-Kaeshi Jyunin-gumi, Mitsui, and Echigoya were the main players, and were designated as official foreign exchange purveyors by the shogunate. In the Meiji era, exchange companies were established in eight locations, including Tokyo, Yokohama and Osaka, in 1869 (Meiji 2). In addition to foreign exchange services, they also issued paper money and handled deposit and loan operations. However, with the subsequent development of the banking system, foreign exchange services came to be mainly handled by ordinary banks. [Kazuo Ota] kindsForeign exchange is classified according to the nature of the transaction as follows: (1) When funds are settled domestically, it is called domestic exchange, and when they are settled internationally, it is called foreign exchange. (2) When classified according to the flow of funds, they can be divided into remittance money orders, in which funds are transferred from a debtor to a creditor (parallel money orders), and collection money orders, in which a creditor collects funds from a debtor (reverse money orders). Remittance money orders can be made by remittance check or by bank transfer, but currently, most of the total amount of money orders handled is by bank transfer. Remittance money orders can also be made by telegraph or by document. (3) When the counterparties to a foreign exchange transaction are within the same financial institution, it is called a head office/branch foreign exchange transaction; when the counterparties are branches of other banks, it is called an interbank foreign exchange transaction. [Kazuo Ota] structureThe parties to a foreign exchange transaction are, in the case of a remittance, the client, the sending bank, the remitted bank, and the recipient, while in the case of a collection transaction, the creditor (the person requesting collection), the entrusting bank, the trustee bank, and the debtor (the payer). Foreign exchange transactions can be between a client and a bank, between a sending bank and a remitted bank, or between an entrusting bank and a trustee bank, but legally, all of these are interpreted as entrustment or quasi-entrustment under the Civil Code. [1] How remittances work First, let's look at how it works when a remittance check is used. This method using a remittance check is often used when there is no business relationship between the recipient and the receiving bank. Here is how it works when client A remits money to recipient B. (1) Client A brings the remittance funds and fees to the sending bank, Bank A, and (2) receives the remittance check. (3) Client A mails the remittance check addressed to Bank B. (4) Bank A sends a regular remittance instruction to recipient Bank B via teletransfer using the Nationwide Bank Data Communication System (abbreviated as the Zengin System), requesting that the remittance check be paid when it is presented. (5) Client B presents the remittance check received from Client A to Bank B, and (6) receives the cash. Next is the transfer method, which assumes that the recipient has a regular savings or current account at the receiving bank. It works as follows: (1) Remitter A asks Bank A to deposit the funds into Recipient B's bank account. (2) Sending bank Bank A notifies receiving bank Bank B to deposit the funds into B's deposit account. (3) Bank B deposits the funds into B's account. There are three types of transfer methods: document transfer, which consists of document transfer by document exchange and email transfer, in which a transfer slip is sent and received by mail, and teletransfer using the Zengin System. Note that a single transfer request form that combines multiple transfers is called a comprehensive transfer. [2] How collection works There are several methods for collection: individual collection, centralized collection, and centralized collection of near-term bills (centralized collection of bills with an imminent due date), but most collections are centralized using a bill collection center (collection center). The following shows how collection works when Party A sells goods to Party B in a remote location. (1) Creditor (requester of collection) Party A issues a bill of exchange and gives it to its corresponding bank, Bank A, requesting collection of the payment from debtor (payer) Party B. (2) Commissioning bank Bank A sends it to its own collection center. The commissioning bank's collection center mails the bill of exchange to trustee bank Bank B, requesting collection of the payment. (3) Bank B's collection center, which has received the collection request, sends the bill to each of the entrusted branches. Each entrusted branch presents the bill to Party B, either directly or by bill exchange, and (4) collects the payment. (5) Bank B's collection center transfers the collected amount to Bank A's collection center through the Zengin System. (6) Bank A deposits the money into the account of the collection requester, A. In this case, A usually entrusts a carrier with the delivery to B, receives a bill of lading or other documents, and issues a bill of exchange using these as collateral. Note that if the transaction between A and B is international, it becomes foreign exchange. [Kazuo Ota] Exchange Trading ContractWhen conducting such exchange transactions, sending remittance information, transfer notices, or bills of exchange for collection to other financial institutions without a prior contract does not give rise to any right to bind the other financial institution. Therefore, when conducting exchange transactions with other financial institutions, a contract is required in advance. This is called an "exchange transaction contract," and the other party to this contract is called a correspondent. Exchange transactions between member banks in Japan's nationwide bank domestic exchange system are conducted based on the "Domestic Exchange Handling Regulations," and by submitting a memorandum of understanding that these handling regulations will be observed, it is treated as if an exchange transaction contract has been concluded between all member banks. [Kazuo Ota] Settlement of foreign exchange loansIn Japan's nationwide bank domestic funds transfer system, the settlement of funds transfers between sending and receiving banks is carried out by collecting telegraphic transfers at the National Bank Data Communication Center (abbreviated as Zengin Center) based on telegrams and debiting or crediting the current accounts of each member bank at the head office or branch of the Bank of Japan at 5:00 pm on the day of the funds transfer transaction. In addition, document funds transfers by exchange are settled by bill clearing. [Kazuo Ota] Foreign ExchangeWhen foreign exchange transactions are conducted internationally, they are called foreign exchange, and the principles are the same as domestic exchange. However, because foreign exchange transactions are conducted between countries with different monetary systems, they are subject to fluctuations in exchange rates and restrictions on foreign exchange policies. In Japan, foreign exchange transactions previously required approval from the Ministry of Finance, but this was liberalized with the enforcement of the Foreign Exchange and Foreign Trade Act (Revised Foreign Exchange Act) in April 1998. [Kazuo Ota] "Q&A: New Domestic Exchange Practices" compiled by the National Bank Data Communication Center (1995, Financial and Fiscal Affairs Research Institute)" ▽ "Matsumoto Sadao, "Introduction to Domestic Exchange Practices" (1995, Financial and Fiscal Affairs Research Institute, Kinzai Publishing)" [Reference] | | | | |©Shogakukan "> How money order works (by money order cheque) ©Shogakukan "> How collection money order works Source: Shogakukan Encyclopedia Nipponica About Encyclopedia Nipponica Information | Legend |

|

隔地者間の金銭上の債権・債務の決済、あるいは資金移動を、現金の輸送をすることなく、第三者である金融機関を介して行う仕組みである。金融機関にとって為替業務は、預金、貸出と並ぶ固有業務の一つとされている。 [太田和男] 歴史こうした為替の仕組みは、ヨーロッパでは12世紀ごろにイタリアを中心とする地中海沿岸の都市で、バンコbancoとよばれる両替商によって行われ始めた。当時イタリアの商業の発達は目覚ましく、貿易も盛んであったが、隔地間取引の決済に貨幣を輸送することは不便であり、危険でもあったからである。さらに12~13世紀の十字軍遠征による人員、物資の大量移動に伴う遠隔地取引の増加によって為替はいっそうの発達をみた。 日本における為替の起源は、鎌倉時代にまでさかのぼることができる。当初は「かわし」とよばれ、その仕組みは、依頼人が割符(さいふ)屋に金銭や米を渡して割符とよぶ為替手形を受け取り、この手形を支払指定地で支払人に渡し、引き換えに金銭や米を受け取るものであった。江戸時代になると、大消費地江戸と、全国的な商業中心地大坂とを結んで資金決済を行う「江戸為替」が急速に発達し、今日の為替の仕組みの原型が完成した。この時代の為替業務は両替商によって行われており、とくに1691年(元禄4)に幕府から御為替御用達の指定を受けた、いわゆる御為替十人組と三井、越後(えちご)屋などが中心となっていた。明治に入ると、1869年(明治2)に東京、横浜、大阪など8か所に為替会社が設立され、為替業務のほかに紙幣の発行、預金・貸付業務をもあわせて行ったが、その後の銀行制度の整備とともに、為替業務は主として普通銀行が担うようになった。 [太田和男] 種類為替は、取引の性格によって次のように分類される。 (1)資金の決済が国内で行われる場合を内国為替、国際間で行われる場合を外国為替という。 (2)資金の流れによって分類すれば、資金を債務者から債権者に送金する送金為替(並為替)と、資金を債権者が債務者から取り立てる取立為替(逆為替)とに分けられる。送金為替には、送金小切手によるものと振込みによるものとがあるが、現在、全為替取扱い量の多くは振込みである。また、この送金為替にはそれぞれ電信扱いと文書扱いとがある。 (3)為替取引の相手方が、同一金融機関内であるときには本支店為替、他行店舗である場合には他行為替という。 [太田和男] 仕組み為替取引の当事者としては、送金為替の場合には、依頼人、仕向(しむけ)銀行、被仕向銀行、受取人が存在し、取立為替の場合には、債権者(取立依頼人)、委託銀行、受託銀行、債務者(支払人)が存在する。為替取引には、依頼人と銀行との間の取引と、仕向銀行と被仕向銀行、委託銀行と受託銀行との間の取引とがあるが、法律的には、いずれも民法上の委任もしくは準委任と解釈されている。 〔1〕送金為替の仕組み まず、送金小切手による場合の仕組みをみてみよう。この送金小切手による方式は、受取人と被仕向銀行との間に取引関係がないときなどに用いられることが多い。依頼人甲が受取人乙に送金する場合の仕組みを示す。(1)甲は仕向銀行A銀行に送金資金と手数料を持参して、(2)送金小切手を受け取る。(3)甲は乙あてに送金小切手を郵送する。(4)A銀行は、被仕向銀行B銀行に対して、全国銀行データ通信システム(全銀システムと略称)利用のテレ為替によって、送金小切手が呈示されれば支払ってもらいたい旨、普通送金取組案内を発信する。(5)乙は、甲から受け取った送金小切手をB銀行に呈示して、(6)現金を受け取る。 次に振込みによる方式であるが、これは、受取人が被仕向銀行に普通預金、もしくは当座預金の口座を有していることが前提となる。その仕組みは次のとおりである。(1)振込人甲は、A銀行に対し、受取人乙の取引銀行の口座に為替資金を入金するように依頼する。(2)仕向銀行A銀行は、被仕向銀行B銀行に対し、乙の預金口座に入金するよう通知する。(3)B銀行は乙の口座に入金する。この振込み方法には、文書交換による文書振込みと郵便により振込み票を授受するメール振込みとからなる文書為替と、全銀システム利用のテレ為替による振込みとがある。なお、複数件の振込みをまとめて1枚の振込み依頼書により行うものを総合振込みという。 〔2〕取立為替の仕組み 代金取立ての方式には、個別取立て、集中取立て、期近手形集中取立て(期日が切迫した手形の集中取立て)があるが、ほとんどは手形集中センター(集手センター)利用の集中取立てにより行われる。甲が遠隔地の乙に対して商品を販売した場合の代金取立ての仕組みを示す。(1)債権者(取立依頼人)甲は為替手形を振り出し、それを取引銀行A銀行に渡して、債務者(支払人)乙からの代金取立てを依頼する。(2)委託銀行A銀行は、それを自行の集手センターに送付する。委託銀行の集手センターは、受託銀行B銀行に対し、為替手形を郵送して代金取立てを依頼する。(3)取立ての依頼を受けたB銀行の集手センターは、手形を各受託店に送付する。各受託店は、直接あるいは手形交換などによって乙に手形を呈示し、(4)代金取立てを行う。(5)B銀行の集手センターは、取り立てた代金を全銀システムを通してA銀行の集手センターあてに資金付替(つけかえ)をする。(6)A銀行は取立依頼人甲の口座に入金する。この場合、甲は乙への送荷を運送業者に委託し、貨物引換証や船荷証券などを受け取り、これを担保として為替手形を振り出すのが通常である。なお、甲と乙との取引が国際間に及んでいる場合には外国為替となる。 [太田和男] 為替取引契約このような為替取引を行う場合、事前に契約なしに他の金融機関あてに送金案内、振込み通知の発信、あるいは取立てのための為替手形を送付しても、相手金融機関を拘束する権利は生じない。そこで、他の金融機関と為替取引を行おうとする場合には、事前に契約が必要となる。これが「為替取引契約」であり、この契約の相手方をコルレス先とよんでいる。日本の全国銀行内国為替制度における加盟銀行間の為替取引は、「内国為替取扱規則」に基づいて行われており、この取扱規則を遵守する旨の念書を提出することをもって、全加盟銀行の間で為替取引契約が締結されたものとして扱っている。 [太田和男] 為替貸借の決済日本の全国銀行内国為替制度における仕向銀行と被仕向銀行の為替貸借の決済は、テレ為替による分については、電文に基づいて全国銀行データ通信センター(全銀センターと略称)で集計され、為替取引の当日午後5時、日本銀行の本支店にある各加盟銀行の当座預金口座から引落しあるいは入金することにより行う。また、文書為替のうちの交換振込みによるものは、手形交換で決済される。 [太田和男] 外国為替為替取引が国際間で行われる場合を外国為替といい、その原理は内国為替と同じである。しかし、外国為替の場合は、貨幣制度を異にする国の間の取引であるから、為替相場の変動や為替政策上の制約などを受ける。日本では、従来、外国為替業務を扱うには大蔵省の認可が必要であったが、1998年(平成10)4月の外国為替及び外国貿易法(改正外為(がいため)法)施行で自由化された。 [太田和男] 『全国銀行データ通信センター編『Q&A新しい内国為替実務』(1995・金融財政事情研究会)』▽『松本貞夫著『実務内国為替入門』(1995・金融財政事情研究会、きんざい発売)』 [参照項目] | | | | |©Shogakukan"> 送金為替の仕組み(送金小切手による場合… ©Shogakukan"> 取立為替の仕組み 出典 小学館 日本大百科全書(ニッポニカ)日本大百科全書(ニッポニカ)について 情報 | 凡例 |

>>: Freshwater pearl oyster - Margaritifera laevis

Recommend

Town Law - Choho

In the Edo period, autonomous regulations were est...

Ushu Tandai

The Muromachi Shogunate's governing body for ...

chemical sensitization

...The process of making a photosensitive materia...

《Kamatari》

...The title of a dance piece by Kowaka. Also kno...

thermal soaring

...The most typical model engine is the glow plug...

Air defense drill - boukuenshuu

〘 noun 〙 Practical training based on actual condit...

Ekishi - Ekishi

...This was a major conspiracy that was called th...

Kuwagatai stone

A type of stone bracelet-shaped treasure made in ...

White lupine

...Those used as feed and green manure include th...

Tagaya - Tagaya

Edo Rakugo has been performed since ancient times....

Wang Gen - Golden

A commoner thinker of the Ming Dynasty in China. ...

Asahi [village] - Asahi

A village in Higashitagawa County, western Yamagat...

Petrovich Avvakum

1620‐82 A 17th-century Russian archpriest. A leade...

Coptic art

Copts are Egyptian Christians, and a general term...

Fujiwara no Kaneie

A nobleman in the mid-Heian period. Son of Morosu...